Legendary investor Warren Buffett is famous for his long-term perspective. He has said that he likes to make investments he would be comfortable holding even if the market shut down for 10 years.

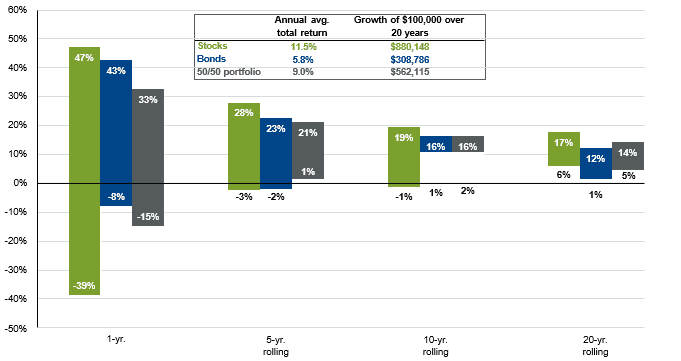

Investing with an eye toward the long term is particularly important with stocks. Historically, equities have typically outperformed bonds, cash, and inflation, though past performance is no guarantee of future results and those returns also have involved higher volatility.

It can be challenging to have Buffett-like patience during periods such as 2000-2002, when the stock market fell for 3 years in a row, or 2008, which was the worst year for the Standard & Poor's 500 index since the Depression era. Times like those can frazzle the nerves of any investor, even the pros. With stocks, having an investing strategy is only half the battle; the other half is being able to stick to it.

Just what is long term?

Your own definition of "long term" is most important, and will depend in part on your individual financial goals and when you want to achieve them. A 70-year-old retiree may have a shorter "long term" than a 30-year-old who is saving for retirement.

Your strategy should take into account that the market will not go in one direction forever — either up or down.

The benefits of patience

Trying to second-guess the market can be challenging at best; even professionals often have trouble. According to "Behavioral Patterns and Pitfalls of U.S. Investors," a 2010 Library of Congress report prepared for the Securities and Exchange Commission, excessive trading often causes investors to underperform the market.

Another study, "Stock Market Extremes and Portfolio Performance 1926-2004," initially done by the University of Michigan in 1994 and updated in 2005, showed that a relatively small number of months or even days account for most market gains and losses. The return dropped dramatically on a portfolio that was out of the stock market entirely on the 90 best trading days in history. Returns also improved just as dramatically by avoiding the market's 90 worst days; the problem, of course, is being able to forecast which days those will be. Even if you're able to avoid losses by being out of the market, will you know when to get back in?

Keep yourself on track

It's useful to have strategies in place that can help improve your financial and psychological readiness to take a long-term approach to investing in equities. Even if your're not a buy and hold investor, trading discipline can help you stick to a long-term plan.

Have a game plan against panic

Having predetermined guidelines that anticipate turbulent times can help prevent emotion from dictating your decisions. For example, you might determine in advance that you will take profits when the market rises by a certain percentage, and buy when the market has fallen by a set percentage. Or you might take a core-and-satellite approach, using buy-and-hold principles for most of your portfolio and tactical investing based on a shorter-term outlook for the rest.

Remember that everything's relative

Most of the variance in the returns of different portfolios is based on their respective asset allocations. If you've got a well-diversified portfolio, it might be useful to compare its overall performance to the S&P 500. If you discover you've done better than, say, the stock market as a whole, you might feel better about your long-term prospects.

Look at performance over longer periods

Don't forget to look at how far you've come since you started investing. When you're focused on day-to-day market movements, it's easy to forget the progress you've already made. Keeping track of where you stand relative to not only last year but to 3, 5, and 10 years ago may help you remember that the current situation is unlikely to last forever.

Consider playing defense

Some investors try to prepare for volatile periods by reexamining their allocation to such defensive sectors as consumer staples or utilities (though like all stocks, those sectors involve their own risks). Dividends also can help cushion the impact of price swings.

If you're retired and worried about a market downturn's impact on your income, think before reacting. If you sell stock during a period of falling prices simply because that was your original game plan, you might not get the best price. Moreover, that sale might also reduce your ability to generate income in later years. What might it cost you in future returns by selling stocks at a low point if you don't need to?

Use cash to help manage your mindset

Having some cash holdings can be the financial equivalent of taking deep breaths to relax. It can enhance your ability to act thoughtfully instead of impulsively. An appropriate asset allocation can help you have enough resources on hand to prevent having to sell stocks at an inopportune time to meet ordinary expenses or, if you've used leverage, a margin call.

A cash cushion coupled with a disciplined investing strategy can change your perspective on market downturns. Knowing that you're positioned to take advantage of a market swoon by picking up bargains may increase your ability to be patient.

Know what you own and why you own it

When the market goes off the tracks, knowing why you made a specific investment can help you evaluate whether those reasons still hold. If you don't understand why a security is in your portfolio, find out. A stock may still be a good long-term opportunity even when its price has dropped.

Tell yourself that tomorrow is another day

The market is nothing if not cyclical. Even if you wish you had sold at what turned out to be a market peak, or regret having sat out a buying opportunity, you may get another chance. If you're considering changes, a volatile market is probably the worst time to turn your portfolio inside out. Solid asset allocation is still the basis of good investment planning.

Be willing to learn from your mistakes

Anyone can look good during bull markets; smart investors are produced by the inevitable rough patches. Even the best aren't right all the time. If an earlier choice now seems rash, sometimes the best strategy is to take a tax loss, learn from the experience, and apply the lesson to future decisions.

This content has been reviewed by FINRA.