Check out our latest blog posts or browse by category.

With potential government seed funding, tax advantages, and flexible future use, these accounts may complement existing savings strategies such as 529 plans. Learn how they work, who qualifies, and key considerations before opening an account.

Retirement is one of life's biggest transitions, yet many couples spend more time planning the finances than discussing what retirement will actually look like. Before you stop working, make sure you're asking the right questions about your future together.

Trump Accounts: A New Opportunity to Invest in Your Child's Future

Receiving a financial windfall can create incredible opportunities—and important decisions. Discover key strategies to help protect, grow, and make the most of unexpected wealth.

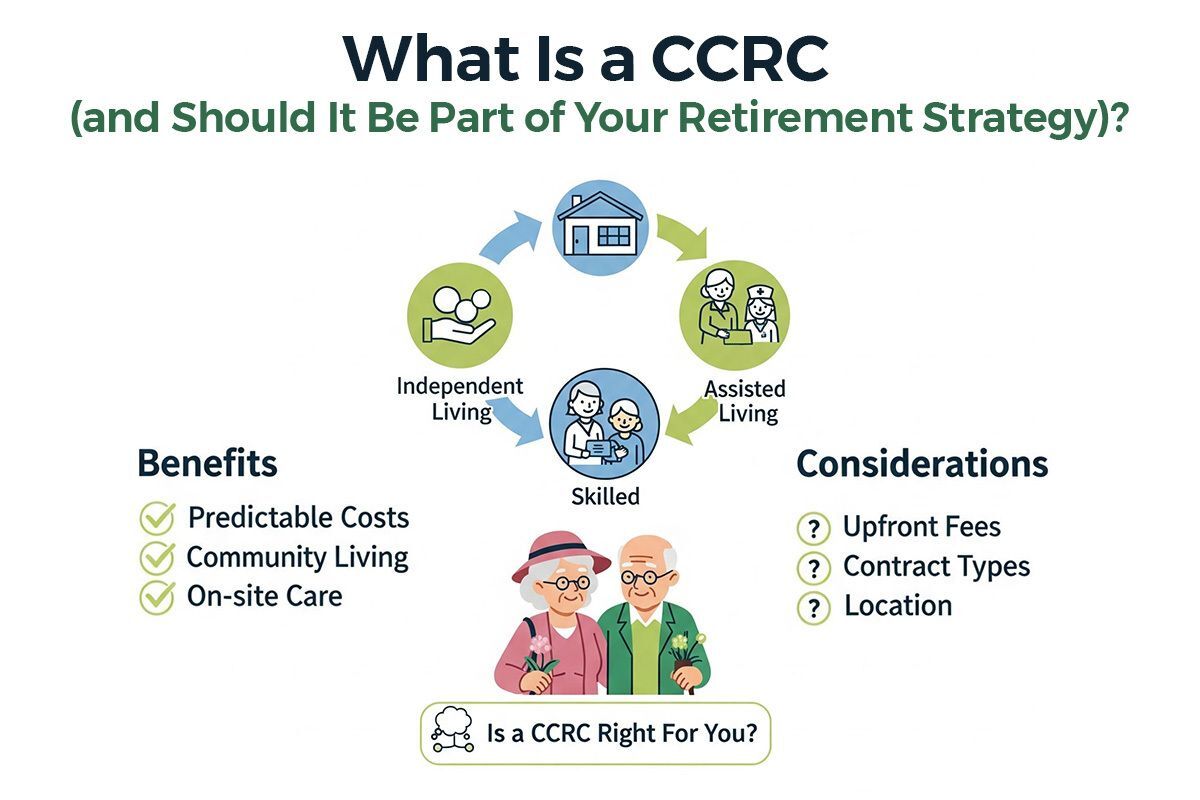

This article explains how continuing care retirement communities (CCRCs) can help retirees proactively plan for housing, healthcare, and long-term care needs while managing financial and family caregiving risks.

How Social Security claiming decisions can impact retirement income, taxes, and long-term financial security.

The importance of proactive financial, legal, and organizational planning to reduce stress and help families better navigate caring for aging parents.

Rising cost of healthcare in retirement and the importance of proactively planning for medical and long-term care expenses as part of a comprehensive retirement strategy.

Subscribe on your favorite app.

Or wherever you listen to your podcasts.